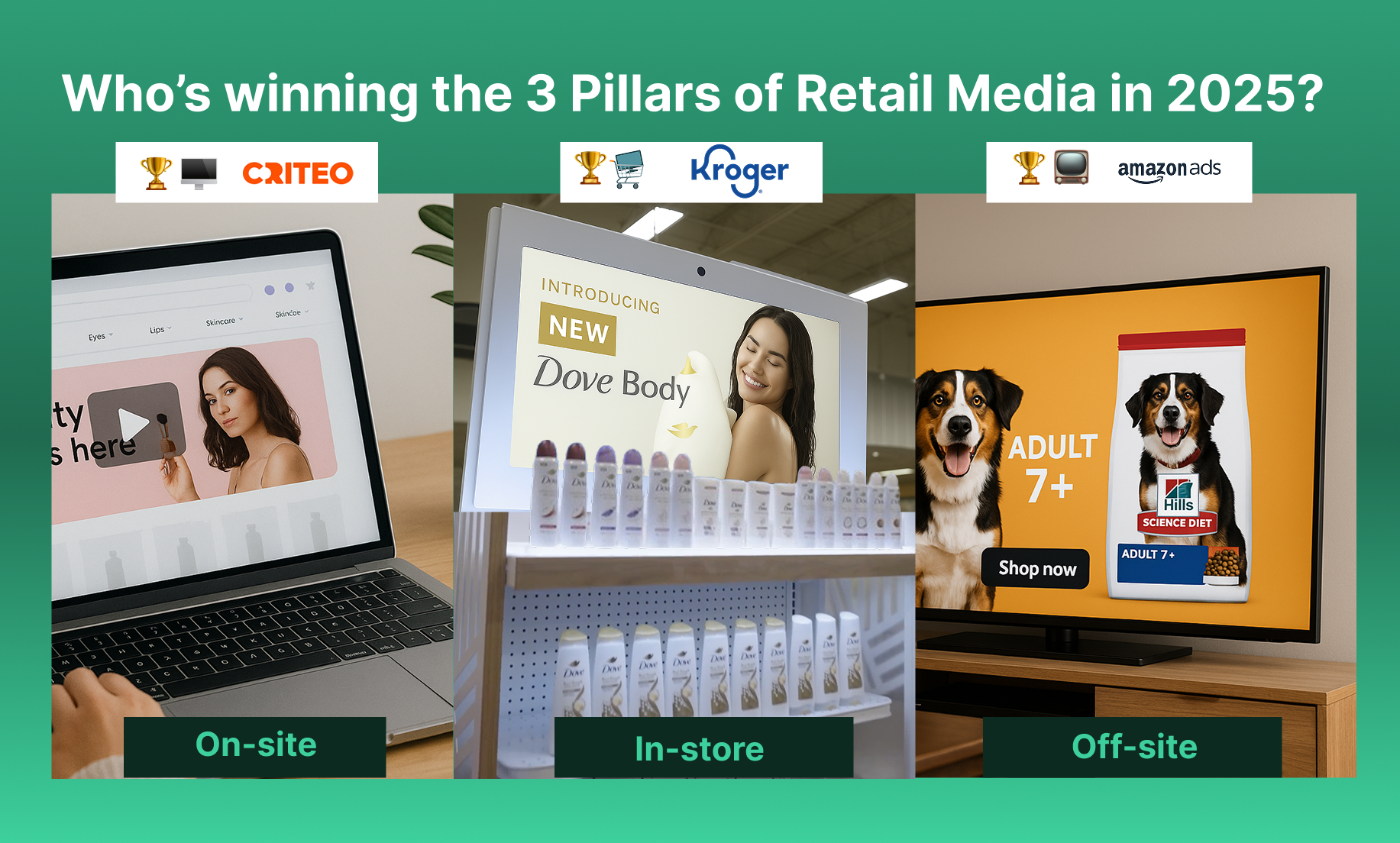

With Kroger’s abrupt CEO change, it’s now time to think about what the next direction is for the largest grocer with respect to the competitive landscape.

First of all, was it really abrupt if they are on the hook for an $800MM breakup fee with Albertsons? Nevermind…whether it was or not, it’s been clear for a while that Kroger and Albertsons are both in a tough spot because neither has the national scale that Walmart has. From our discussions with companies in the #RetailMedia space, we’re seeing two paths diverge: the Amazon Ads model of retail media and the Walmart Connect model.

If we consider the Amazon model, that’s a platform model where a marketplace of sellers uses vast amounts of data to improve the performance of items. In a report from Flywheel called "The Big Shift," they state boldly that “Data is power. If retailers want to differentiate their position, they will be forced to give this data away.” They also argue that retailers need “the most unique selection in order to win the consumer.” If we consider that sponsored product listing ads are the core of retail media—as they have been, benefiting Amazon’s unlimited digital aisles—then this model is clear: brands need access to as full a picture as possible.

That vision aligns well with our recent episode featuring Ramendra (Ram) Singh, Ed. D. from Horizon Media's Night Market , where he demoed his new multi-retailer media optimization platform, NEON. This is the first tool from agencies that truly accounts for retail media networks. Previously, all platforms operated within their own silos. Will iROI become the new metric brands demand, replacing iROAS from the retailer’s own reporting? Will this new multi-retailer approach provide enough channel coverage to truly offer a full picture, or will it mainly serve product listing ads?

On the other hand, there’s Walmart’s approach. While Walmart may aspire to build a vibrant marketplace like Amazon, they have a distinct market positioning: they always own the data and develop products that help brands leverage that data—to the detriment of data syndicators like Circana. About ten years ago, Walmart embarked on a journey to develop the Scintilla (neé Luminate) CDP (see Kiri Masters' dive on the rebrand here) with the help of dunnhumby technology. From Walmart’s perspective, as a national retailer, brands should gain sufficient insights solely from Walmart shoppers' behavior—and it’s hard to argue with that logic.

But what happens if Kroger takes a cue from Walmart and similarly distances itself from data syndicators, lowering the cost of retail intelligence while nudging brands to shift that spend into Retail Media? Brands like PepsiCo, which today invests roughly $90MM annually in retail intelligence, may find the value proposition of Circana and other data aggregators diminishing without Kroger’s dataset.

Does it make sense for Kroger to adopt Walmart’s verticalized model, emphasizing the basket over the item, and prioritizing omnichannel and physical retail over purely online strategies? From our discussion with David Johnson, CEO of Thrasio, it’s clear that physical-first retailers struggle to attract insurgent brands. Many emerging, trend-driven brands resist traditional retail listing rules and planning, finding retailer pricing structures to be a major hurdle. If Kroger and their 84.51˚ data unit move towards a Walmart-like strategy, will it inadvertently create barriers for these innovative brands, or could it redefine the retail intelligence ecosystem to support a more dynamic and competitive marketplace?

In lieu of the flashy screens or overwhelming tech, these are intentionally low-tech branding opportunities: lean and focused on the products inside the aisle, where paper promotions are quickly changed daily or weekly. The branding frames the shopping moment, and then promptly gets out of the way.

The industry can often equate innovation with complexity — this is a good reminder that lean doesn’t necessarily mean lazy, but rather disciplined.

It’s not every day that a competitor spills their secrets: Mark Williamson, AVP of Retail Media at Costco, took an opposite approach to all other retailers by revealing exactly which vendors power his RMN stack at NRF 2026.

Costco’s RMN tech stack includes:

(image)

This level of transparency is rare, but it’s intentional — and hopefully can serve as a blueprint for the future as retail media matures, and credibility starts to matter more than ever.

As Kiri Masters says in her breakdown of Williamson’s presentation at The Drum:

“Retailers maintaining secrecy should ask themselves: what are we really protecting? And is it worth the cost in advertiser trust and ecosystem collaboration?”

Sarah Marzano recently presented surprising results from her Retail Media Network (RMN) leadership survey.

Historically, RMNs often lived under the Chief Merchandising Officer. But today, RMN leadership is increasingly moving towards roles such as:

CFO being on this list is a particularly recent development, and quite telling: retail media is no longer just about placement and partnerships, but also revenue accountability and strategy.

Something else worth noting: RMNs who are led by a Chief Data Officer or a Head of Ecommerce tend to have a more online or direct-to-consumer focus than those with a more physical presence.

(image)

4. Be focused and ruthless

Quick case study: 7-Eleven’s Gulp Media Network featured real in-store audio creative from brands Phorm Energy and Celsius Live Fit.

Both energy drinks ran in-store audio ads, however Phorm had a much higher lift than Celsius.

Why? As Mario Mijares, VP Marketing, Loyalty, and Monetization Platforms at 7-Eleven explained, it came down to being ruthless about the job to be done in a limited amount of time.

Brands can’t just repurpose their CTV or Linear creative into an in-store audio ad and hope for the best. The winning creative stripped away everything unnecessary and focused on a single, clear message designed for the moment shoppers were actually in. Again, discipline makes all the difference!

New formats and platforms come and go, but intentionality is the reigning theme among all: